With the housing market in crunch, homeowners continue to make investments into their existing properties, using maintenance and remodeling to extend their comfort and livability for the foreseeable future.

A majority of homeowners are willing to take on at least a portion of home improvement activities on their own, hiring contractors and other industry professionals for more complex and large-scale projects.

The Farnsworth Group and the Home Improvement Research Institute (HIRI) partner together to study the activities and sentiments of homeowners and pros on a quarterly basis. The results are published in the Quarterly Homeowner Activity Tracker and the Quarterly Contractor Activity Tracker, and they give insight into homeowners’ and professionals’ attitudes and motivations driving home improvement initiatives.

As a building products manufacturer or supplier, this data can inform your go-to-market strategies in 2026 and help you engage with your customer base, whether it consists of DIY homeowners, industry professionals, or both.

What are Key Home Improvement Trends in 2026?

From an industry standpoint, there hasn’t been any major shifts in how professionals and homeowners are approaching home improvement activities and purchasing products in light of the current economic and cultural landscape. Both groups are showing tempered optimism and a steady approach to home improvement, although challenges related to the costs of materials and labor and other financial uncertainties continue to persist.

Early forecasts paint 2026 as fairly similar to 2025 in terms of industry challenges and opportunities and how both DIY and DIFM homeowners are planning to invest in home improvement in the coming months.

Home Improvement Trends Among Trade Professionals

The construction industry is constantly evolving, shaped by economic conditions, market shifts, and industry-wide challenges. Here are some of the economic and industry trends that are impacting the sentiments and behaviors of contractors and other trade professionals:

1. Project Pipelines are Up Slightly Compared to Q1 2025

Project pipelines have remained relatively steady over the past year, but they are stronger in the first quarter of 2026 than the same period last year. This pertains to the average number of:

- Projects bid on

- Projects awarded

- Projects started

- Projects completed

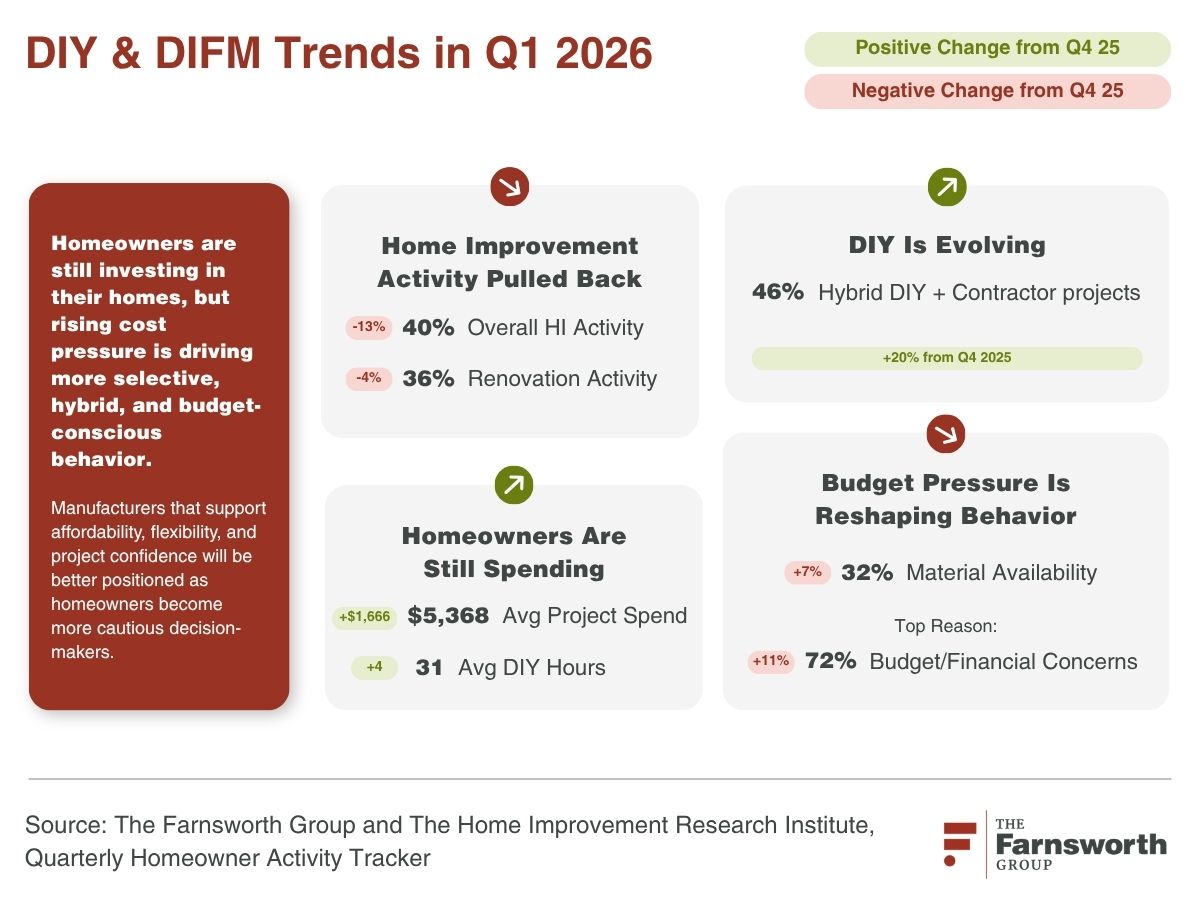

In Q1 2026, the average number of projects that contractors had bid on in the past three months was 15 (compared to 14 in Q1 2025). The total number of projects started was 8.8 and the total number of projects completed was 8.1. However, there was a significant spike in the number of project delays and cancellations, jumping from 31% in Q4 2025 to 54% in Q1 2026. The main drivers of cancellations and postponements continue to be material availability (for 31% of projects) and schedule/timing (for 30% of projects), but budget became a much bigger driver of postponements and cancellations, jumping from 15% in Q4 2025 to 28% in Q1 2026.

2. Economic Uncertainty and Inflation Dominate Concerns

The economy is causing concern for more than half of contractors, according to data from Q1 2026. About 49% also are worried about inflation and how it will impact their business over the next 12 months.

Materials-related challenges also continue impacting contractors, although there was a small drop off in product/material challenges to begin the year. About 41% of contractors cited this as an area where they experienced challenges in the first quarter of 2026, compared to 50% or more in every quarter of 2025.

Among contractors and industry pros who faced material challenges:

- 78% struggled with cost

- 55% struggled with availability

- 34% struggled with quality

3. Labor Availability, Quality and Cost Remain Challenges—but Less Pressing

Labor is another significant macroeconomic challenge for contractors, but availability and quality aren’t driving project cancellations and postponements like they have in the past. In the first quarter of 2026, 38% of contractors claimed they experienced labor-related challenges. However, only 11% of contractors cited availability of labor as a driver of project cancellations and postponements, compared to 24% in Q1 2025. Labor quality affected only 8% of projects, as opposed to 23% in Q1 2025. Among those with labor challenges in the first quarter of 2026:

- 51% struggled with availability

- 49% struggling with cost

- 39% struggled with quality

Training and retention have also become less challenging for contractors. About 27% cited training as an issue, compared to 34% in Q1 2025, and only 19% cited retention as a challenge, compared to 39% in Q1 2025.

4. Professional Contractors Show Steady Optimism

Despite economic and industry challenges, a majority of contractors express some level of optimism about the future. About 56% of contractors expect the home improvement market to grow over the next 12 months, and about 62% also anticipate revenue growth, which is comparable to sentiments that were expressed during this time last year. The areas where pros are expecting growth opportunities include:

- Technology integration

- Energy efficiency improvements

- Expansion into geographic markets

In the first quarter of 2026, contractors were split pretty much 50-50 on how they expect the competitive nature of the market to shift in the next 12 months.

Home Improvement Trends Among DIY and DIFM Homeowners

In order to access the DIY market, it’s important to understand its demographics, as well as the motivations, behaviors and trends influencing different groups within the market. Let’s unpack this group of home improvement product buyers.

1. Overall Home Improvement Activity Drops to Start 2026

In the first quarter of 2026, home improvement activity competed in the past 90 days had decreased to 40%, compared to 53% in Q4 2025. In general, maintenance and repairs continue to be the leading forms of home improvement activities. In the first quarter of 2026, about 74% of homeowners reported having completed a home maintenance project in the past 90 days, down from 78% in the same period last year. Home repairs remained steady, with 68% of homeowners completing projects compared to 69% in Q1 2025. Home renovations—which includes more complex updating and remodeling—were done by 36% of homeowners, down from every quarter of 2025.

2. Skill Capability and Cost Continue to Motivate DIY

There has been a decline in pure DIY activities, as homeowners increasingly combine self-performed work with contractors to manage cost, complexity and execution. In Q1 2026, about 39% of home improvement activities were completed on a DIY basis (with occasional assistance from family, friends, or other non-paid help), down from 48% in the same period of 2025. The percentage of homeowners who hired a contractor in Q1 2026—the DIFM segment—also declined, dropping to 15% from 27% in the previous quarter. Meanwhile, about 46% of homeowners used a hybrid option, integrating a contractor or trade professionals for part of the work and then pitching in some of their own labor. This was a significant jump from 2025, when roughly 20% to 26% used a hybrid method throughout the year. For two-thirds of homeowners, they DIY simply because they have the skills and ability to do the work themselves. About 70% also felt it was cheaper if they did the work themselves (an increase from 76% in the first quarter of 2025). A significant number also enjoy the work. The main challenges they faced when hiring a professional included:

- Too expensive (25%)

- Too busy/unavailable (21%)

- Trustworthiness (21%)

3. DIY Hours and Spending Increase in 2026

In the first quarter of 2026, the average amount of dollars and time spent on home improvement activities was up from every quarter in 2025, which could also be indicative of inflation and the rising cost of materials and products. The average spend among those completing projects was $5,368 (up from $3,957 in Q1 2025) and the average DIY hours was 31 (a decrease from 35 in Q1 2025, but up from the prior two quarters). A majority of homeowners are paying for projects with cash, which has been a steady trend over the past year. Credit cards are also used for about one-quarter of projects.

4. Homeowners Express Strongest Optimism About Smaller Projects

Facing financial challenges and increased cost of living, homeowners are more positive about starting a home improvement project under $5,000, with 35% saying it’s a good time to do so and 32% feeling neutral. Meanwhile, only 22% feel it’s a good time to start a project in the $5k to $25k range, and 50% feel it’s a bade time. Approximately 16% of homeowners believe it’s a good time to start a project in $25k-plus range. When it comes to hiring a professional:

- 21% of homeowners feel it’s a good time

- 32% of homeowners feel neutral

- 47% of homeowners feel it’s a bad time

Looking ahead, the average spending for home improvement activity is being driven by major renovations, indicating that higher-capacity homeowners continue to invest, despite uneven project intent. The data shows resilience in highly discretionary and necessary projects, while moderately elective project intent declines. Here are where homeowners’ intentions sat at the beginning of 2026:

- 72% planned interior work

- 56% planned exterior envelope work

- 51% planned yard, garden, and outdoor work

- 28% planned mechanical- or systems-related work

- 16% planned major renovations

Looking Ahead to Customer Behaviors in 2026

These broader trends reveal how the home improvement market progressed throughout the year. But what about your customers specifically? Effectively strategizing for the future starts with getting a deep understanding of your customer, their purchase drivers, and how they compare options when making a purchase decision.

The Farnsworth Group specializes in custom research tailored to the building products and home improvement markets, helping businesses make data-driven decisions. Our team provides building product manufacturers and suppliers with customized research specific to their needs to better understand DIY, DIFM and professional customers. We also provide the industry with a pulse on DIYer and pro sentiments and through our annual Building Products Customer Guide. This data can help you look forward to how the home improvement industry is likely to evolve—and how it will stay the same—in the coming years.