As we look toward 2026, the single-family housing market is navigating a more tempered path, marked by downward-trending start forecasts and shifting consumer behavior. Builders, economists, and industry analysts are recalibrating expectations amid elevated borrowing costs, constrained migration, and the continued strength of the multifamily segment.

Builder Confidence: Declining with Demand

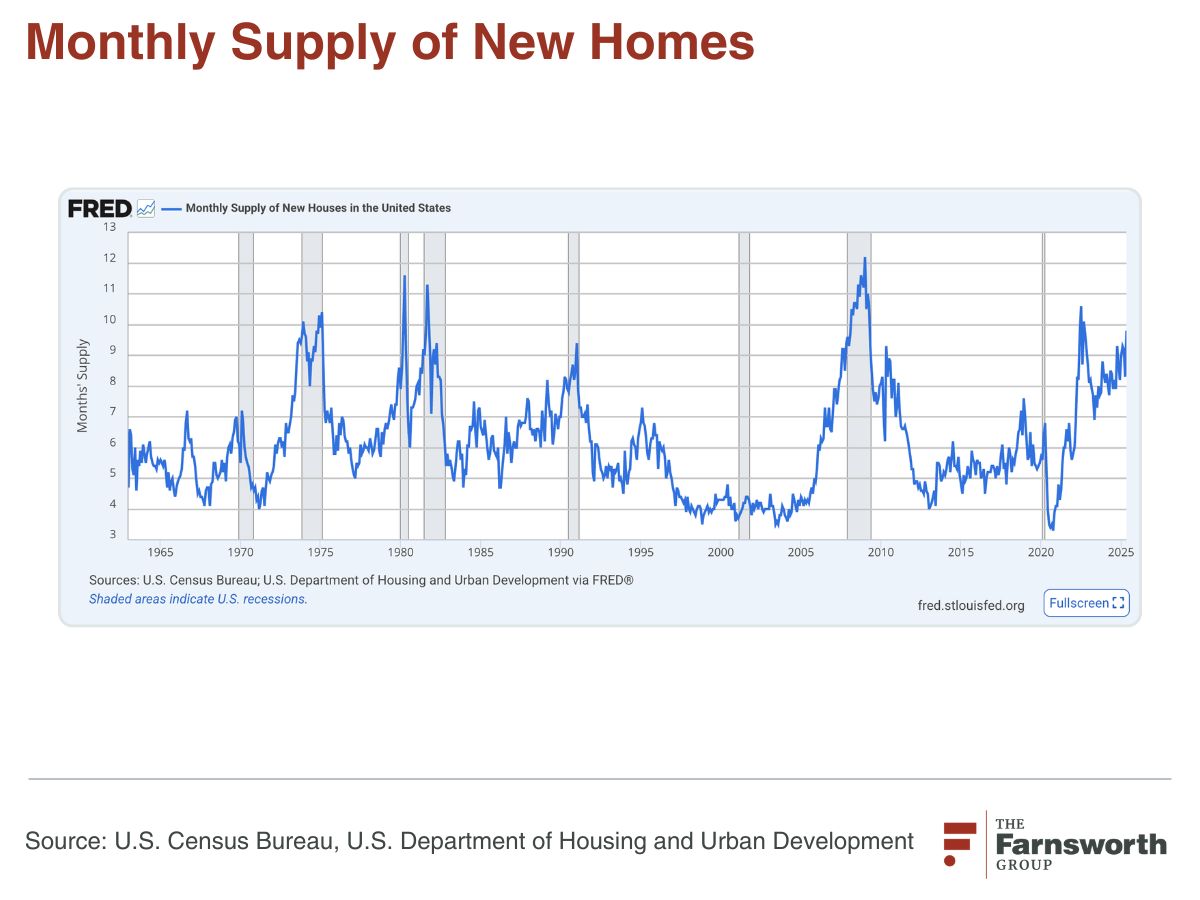

Weak buyer traffic has led to record-high new home inventories. The latest FRED numbers show 9.8 months of new home supply in May 2025 - Historically a number only reached during a recession, with two recent exceptions.

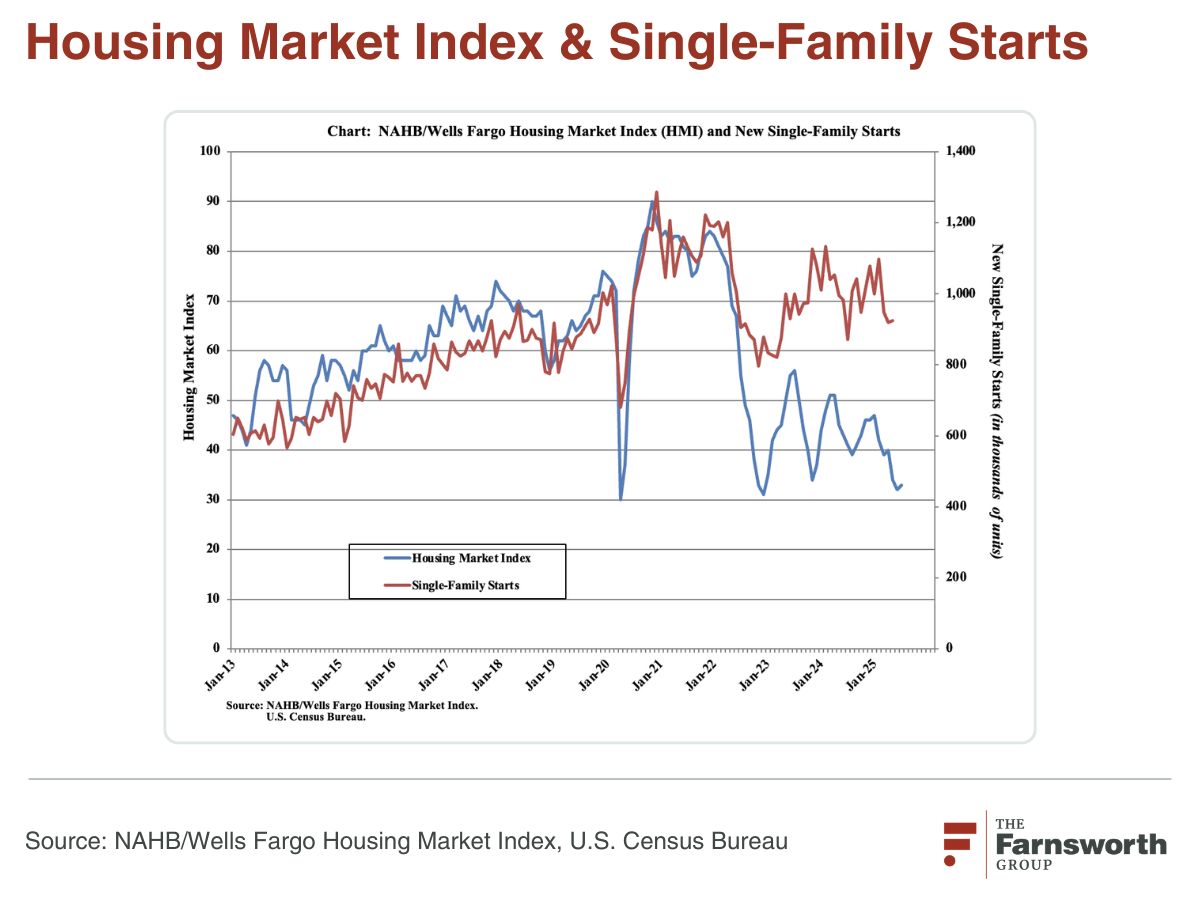

Commensurately, builder sentiment has settled at historically low levels. In June 2025, the NAHB/Wells Fargo Housing Market Index dipped to 32 - only the third time it’s been this low since 2012 - reflecting weak buyer traffic and sales conditions. The June drop followed a further one‑point rise to 33 in July, still well below the 50‑point threshold of builder optimism. Contractor confidence has followed the same declining trajectory.

Builder Discipline Leading to Fewer Active New Single-Family Building Permitting and Housing Starts

With demand under pressure, around 37% of builders cut prices in June, and 62% offered buyer incentives - rates unseen before June 2022. It is clear from home builders that there is a strong desire to get new home inventory down to more reasonable levels before engaging in new starts.

Permitting activity supports this hypothesis. According to data released by the U.S. Census Bureau and HUD, the seasonally adjusted rate of building permits as of June of 2025 was 1,397,000 - 866,000 of which are for single family residential construction. Single-family permits were down 3.7% from the prior month - May 2025 - and down 8.4% from last year - June 2024.

Permitting is a leading indicator to understand the supply of new homes that will be available in the next 8-12 months.

As of May 2025, the U.S. Census Bureau estimates that that 623,000 new single-family houses were sold at a median sale price of $426,600, while currently there are 507,000 new houses for sale.

Many firms have used this data to continually revise down forecasted single-family housing starts throughout the year. In late 2024, most forecasts predicted a slight increase in 2025 starts. Each quarter this forecast has declined, now ranging anywhere from -2 to -12% versus 2024.

Where to Look Now? Active New Multi-Family Building Permitting and Housing Starts & Remodeling Activity

While single-family projections are muted, the multifamily sector is outperforming expectations, lifting overall housing starts. According to data released for June 2025 by the U.S. Census Bureau and HUD, the seasonally adjusted multi-family permits (2+ units) were projected at 531,000 permits.

Permits issued for 2-4 unit multi-family projects showed no change from the month prior - May 2025 - but increased 10.4% from the year prior - June 2024.

In May, permits issued for 5+ unit multi-family projects increased 8.1% compared to May 2025, but only increased 2.1% compared to the year prior - June 2024.

According to the FRED, Multifamily starts jumped 52% year-over-year in June, driven by strong demand for rental units and increased investment in urban infill and mixed-use development. This surge has reshaped the construction landscape, taking pressure off the single-family market while providing an outlet for developers facing land or financing constraints.

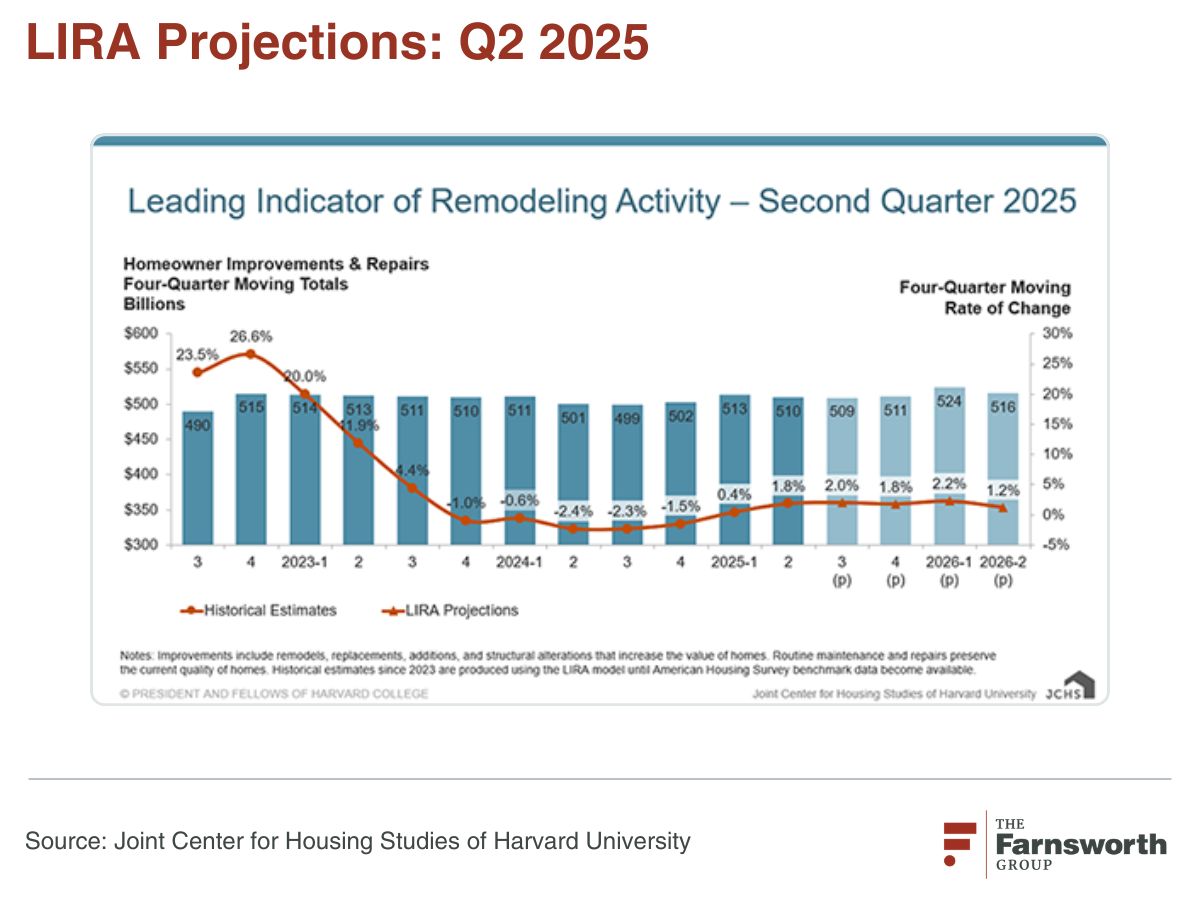

In addition to multifamily, remodeling activity is still projected to increase (albeit not as drastically) in 2025. Although a previous major driver of remodeling activity, homeowner mobility, has declined sharply as many are locked into sub‑4% mortgages, there is an expected uptick in homeowners choosing to “stay and improve.” With the median age of U.S. housing now at 43 years, the demand for remodeling based on maintenance and lifestyle upgrades is accelerating. While overall growth remains slow, discretionary renovations (such as kitchen updates, outdoor living enhancements, and energy efficiency improvements) are picking up as homeowners redirect resources toward improving rather than relocating.

Key Takeaways for 2026

- Single-family starts will slow, signaling continued caution from builders and a greater need to compete for building products manufacturers.

- Multifamily strength will continue to offset single-family softness, maintaining momentum for total housing construction.

- Remodeling demand is shifting from transaction-driven to lifestyle-driven, as migration slows and homeowners invest in place.

As we help our clients navigate this complex environment, it’s clear that nuanced, market-specific insights are more valuable than ever. Whether you’re tracking builder sentiment, product demand, or homeowner behavior, 2026 will require a sharp focus on how changing motivations and economic conditions intersect with residential construction trends.

To chat 1:1 with our team about the latest industry drivers and trends, click below.