Heading into 2026, the residential building and home improvement market is going through a period of being fundamentally sound but operationally strained.

Several of the current underlying demand drivers in the market—including household formation, an aging housing stock, long-term homeownership aspirations, and high home equity—remain intact.

However, near-term activity is constrained by affordability pressures, elevated interest rates, labor and material challenges, and, critically, consumer uncertainty and low disposable income. The result is a market that is neither collapsing nor accelerating, but instead moving forward in a flat, measured way.

For building materials manufacturers and suppliers, these construction industry trends present unique opportunities to rethink your offerings’ perceived value to customers. Retaining customer loyalty will be as much a measure of success in the years ahead as acquiring new customers.

What is the Macro-Economic Outlook for 2026?

There are several factors that shape the outlook for home-building firms and home improvement contractors, including the general state of the economy.

Here is a closer look at the macro-economic factors currently affecting the building materials industry and the 2026 outlook for builders, remodelers, and general contractors:

1. National Economy Continues Contracting

The national economy has been lagging for the past couple of years. However, decline lessened during the second half of 2025, based on The Conference Board's Leading Economic Index (LEI), which takes into account a variety of important indicators. The index declined by 0.3% in November, after declining by 0.1% in October, driven in large part by weak consumer expectations. According to data from The Conference Board, the LEI declined by 1.2% between May and November, which was more moderate than the 2.6% dip from November 2024 to May 2025. Based on current indicators, the U.S. economy will continue to slow down in 2026.

2. The Rate of Inflation is Steady, but Prices Remain High

The Consumer Price Index for all items rose 2.7% from December 2024 to December 2025, while the index for shelter specifically rose 3.2% in the same period, according to data from the U.S. Bureau of Labor and Statistics. While the annual inflation rate has remained steady at 2.7% over the past several months, overall prices for consumer goods are still significantly elevated. Families and individuals across the country are feeling the pressure of high prices, which causes them to be more frugal with purchases and make tradeoffs that influence where and how they spend money.

3. Consumer Confidence is Low

Consumer uncertainty and low disposable income are suppressing activity. Consumer confidence and future expectations are at near-record lows, and nearly three-fourths of consumers believe it is a bad time to buy a home. This may be a reflection of low levels of disposable income, which our research has shown correlates highly to home improvement spending. This psychological drag translates into postponed or canceled projects, reduced project scopes, putting pressure on budgets, and slower decision cycles-often regardless of actual need. For the past five years, our researchers at The Farnsworth Group have tracked DIY activities and Pro activities on a quarterly basis, and will continue to track each's activities throughout 2026.

What is the Housing Market Outlook for 2026?

High mortgage rates, elevated home prices, increasing material costs, and borrowing costs have reduced buying power, particularly for first-time buyers and younger households. Even as rates show signs of softening, homeowner mobility continues to decline, slowing both home sales and the downstream activities that typically follow.

Looking deeper into the construction and remodeling industry, here are some current trends and forecasts related to key indicators in the housing market:

1. Housing Prices

New home sales prices are increasing. At the end of 2025, they were up 4.7% from July and up 1.9% from August 2024, according to data from the Home Improvement Research Institute’s Economic and Industry Update Report for January 2026. While existing home sales prices decreased 1.4% from October to November, they are up more than 1% from the same period last year. Rising home prices, along with higher interest rates continue to make it more appealing to invest in home improvements instead of moving, which is expected to drive growth in the remodeling market.

2. Single- and Multi-Family Home Builds

Housing starts refers to the amount of new residential construction projects beginning each month, and they serve as an important indicator of the health of the housing market, in general. Here is a look at the activity that took place in 2025 and the forecast for this year:

2026 Outlook for Single-Family Starts

Single-family permits, starts, and completes—a leading indicator of future construction activity—declined in 2025 compared to 2024 as costs increased, along with elevated mortgage rates. This continues to increase the national problem of under-building SF homes.

According to curated data from National Association of Home Builders (NAHB) in The Farnsworth Group’s Construction and Remodeling Industry Drivers and Forecast Study, single-family starts will remain steady throughout 2026 before starting to recover in 2027. These new home starts will add a much-needed increase to housing inventory.

2026 Outlook for Multi-Family Starts

Meanwhile, multi-family construction reaped the rewards in 2025 in response to declining single-family housing starts. About 410,000 MF home starts were forecast for the entirety of 2025, compared to 355,000 in 2024. Additionally, permits for new MF construction have remained relatively steady.

Looking ahead, multi-family housing is expected to moderate in 2026 and even decrease slightly in 2027 as supply levels begin to balance the market.

3. Housing Inventory Levels

Both the new and existing home supply gap continues to be wider than normal at the start of 2026. In particular, the existing home supply remains noticeably low, although it is projected to improve in the coming months. There is a roughly four-month supply of existing homes, while a six-month supply is considered healthy. Higher new home inventory creates more aggressive tactics to move inventory and may cause builders to defer new starts. Another trend that likely will affect the remodeling and home improvement outlook for 2026 is that the median age of owner-occupied houses is now 43 years, rising steadily since the Great Recession. Older homes need more maintenance and upgrades, driving growth in the remodeling, repair, and maintenance market.

4. Housing Affordability

Housing affordability also plays a role in the housing market fundamentals. Currently, the Housing Affordability Index, which measures whether an average family can afford the the median home, remains at 20-year lows, primarily because of high home prices and high mortgage rates. Although the index increased in the fall, the improvement was relatively small compared to the depth of the decline. As affordability remains near a generational low, would-be buyers are delaying their purchase.

First-time homebuyers have been stretching for the past several years to afford payments, and both builders and smart resellers have been significantly helping with the challenge facing these buyers who need to either amass a sizeable down payment, get a break on interest rates, or ideally both.

Affordability, high home prices, low inventory and high home equity also continues to reduce mobility rates by keeping homeowners in their homes. 2024 saw the lowest mobility rate in the past 20 years, down to nearly 8% of households moving during the year. This will result in more existing home projects as the housing stock ages and homeowners have few options but to remodel their current home.

Diving Deeper: First-Time Homebuyer Scenario

As of July 2025, the most up-to-date information from the U.S. Census Bureau and U.S. Department of Housing and Urban Development (HUD), the median sales price of a home in the United States was about $410,800 and a conventional 30-year mortgage could be secured for about 6.138% mortgage rate for the typical borrower. Assuming the purchase price of the home is $410,800 and the loan term is 30 years, here’s a look at what a first-time homebuyer’s monthly payment outlook is based on a simplified range of options they have in the current market:

- 3% ($12.3k) Down, 6.138% APY = $2,425/mo

- 20% ($82k) Down, 6.138% APY = $2,000/mo

(Note: This simplified look does not include other compulsory monthly costs, such as PMI, insurance, and taxes.)

At an option where the monthly minimum payment is nearly $2,425/month plus additional, compulsory cost of ownership line items, the typical household needs to earn roughly $130,000 per year in order to responsibly enter the current housing market. This means only households in the top 20% of income earners can currently afford an average home in current market conditions.

How to Keep New Home Inventory Moving in 2026

The above simplified look at first time homeowners' options makes it clear why the move to offer rate buy-downs by public builders especially, has been keeping housing stock moving despite the high house prices and high-interest rate market environment. Builders have been responding to sales pressures by cutting prices and offering sales incentives.

Thus, any sort of market changes in 2026 that create options for homeowners to get into the market more favorably (i.e., job creation, lower inflation/interest rates, lower home prices, more housing inventory) will drive increased demand, and any continued market changes that add more strain (i.e., job losses, higher inflation/interest rates, higher home prices, less housing inventory) will drive decreased demand.

5. Home Sales

All this in mind, if makes sense why sales of existing homes are down substantially year-over-year because of rising interest rates and high costs coupled with low consumer confidence, economic uncertainty, and a large shortage of inventory. One of the leading indicators of home sales activity is the Mortgage Market Index (MMI), provided by the Mortgage Bankers Association of America. From November 2020 to December 2025, the index has dropped from over 800 to about 300. On a positive note, the index has been slowly creeping back up into the 300s after spending much of the past three years in the 200—and even 100—range.

6. Building Materials and Products Costs

Since 2020, there has been a notable rise in costs for key construction materials. While declines in demand caused some prices to fall a bit throughout 2024, they jumped back up in 2024. The Federal Reserve Bank’s Producer Price Index (PPI) for Construction Materials rose from approximately 326 at the start of 2025 to about 339 in November. In particular, year-over-year costs for iron and steel have, more or less, leveled out since spiking in 2021, with marginal inclines and declines over the past year. has seen a significant decline in year-over-year costs, while materials such as ready-mix concrete are still high.

Opportunities and Challenges Faced by Industry Pros

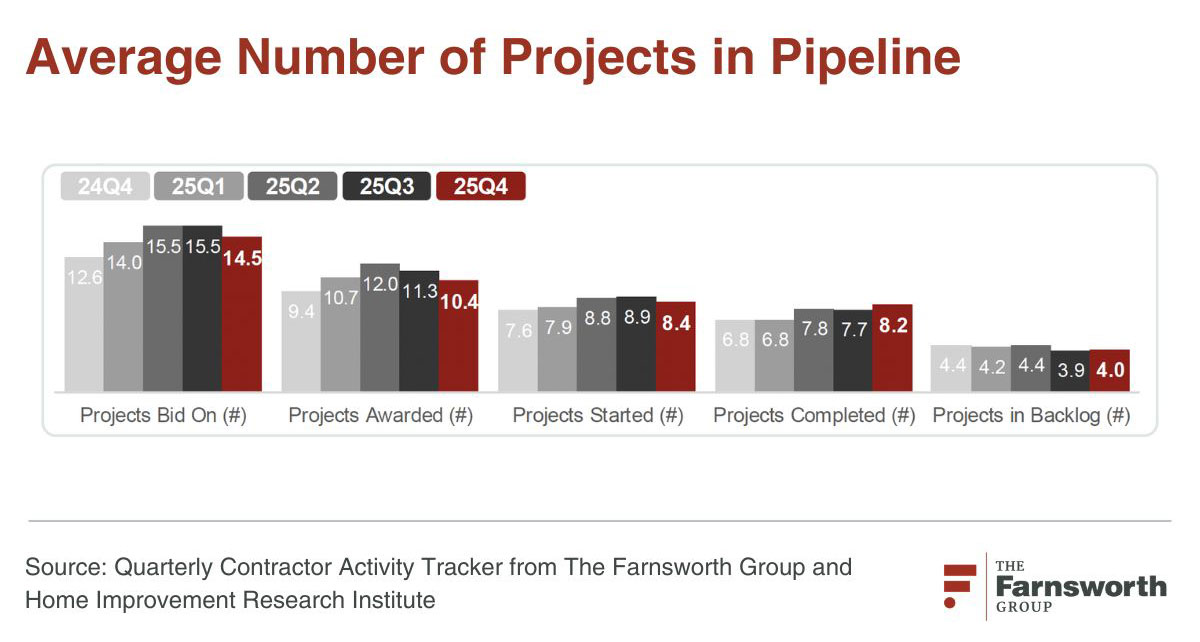

Contractors across specialties have been staying busy in 2025. According to our findings in the Quarterly Contractor Activity Tracker, the entire project pipeline increased from Q4 2024 to Q5 2025, except project backlog. This includes projects bid on, projects awarded, projects started, and projects completed.

Some of the main drivers of project cancellations and postponements include schedule and/or timing; material availability; and a decision by the homeowner. Over the past couple years, securing skilled labor has also become an increasing challenge, in terms of availability, costs, and quality. In particular, availability of labor increased significantly as a driver or project cancellation and/or postponement from the fourth quarter of 2024 to the fourth quarter of 2025.

This is a reflection of the state of the workforce on a larger scale. Data from the U.S. Bureau of Labor Statistics shows that participation in the workforce has steadily declined for nearly two decades. After falling dramatically during the COVID-19 pandemic, participation is on a steady rise, but well below what is needed. Approximately 39% of contractors feel there is a need for a stronger focus on training, highlighting the workforce development challenges they’re facing.

In general, competitiveness lifted slightly in 2025, with only 18% of contractors noting significantly more competition in Q4 2025—down from 21% in Q4 2024. Even still, contractors are demonstrating a tempered sense of optimism. About three in five anticipate the home improvement market will grow throughout 2026, while 10% believe it will decline significantly. Efficiency, technology and sustainable materials are perceived as the primary drivers of growth. Nearly two-third of contractors also anticipate revenue growth in the next 12 months.

Furthermore, data from The Farnsworth Group’s separate Quarterly Contractor Index shows steady confidence among remodelers, mechanical contractors, finish contractors, exterior contractors, and landscape contractors, who all are staying busy with healthy backlogs across the board. Many companies are booked out between eight to nine weeks in advance.

The biggest growth opportunities for homebuilders and contractors include energy efficiency and renewable energy installations and technology integration.

Planning for Home Builders’ Needs in 2026

Industry professionals have to become strategically flexible in order to navigate the dynamic—and sometimes rapidly changing—housing market and the various macro-economic forces that create an impact on housing. Buyer sentiment has created an environment where contractors must compete more fiercely to win new business.

When dealing with both manufacturers and suppliers in the construction materials market, contractors frequently cite product availability and delivery times as their primary challenges.

What we heard from our live Pro panel at the 2026 Building Products Customer Workshop is that the dealer channel remains important for Pros, as dealers are often the first point of contact for pros seeking product answers and recommendations, and manufacturers should be intentional about equipping dealers to serve that role.

As with specialty trades, training and empowerment came up repeatedly. Dealers want the ability to fix problems quickly without layers of red tape, and they value manufacturers who invest in equipping their teams so they can better serve Pro customers.

In terms of what specifically manufacturers can be doing to improve performance through dealer channels, one panelist summarized it best: “It’s no one thing manufacturers need to do, it’s the culmination of things.” Brands that consistently show up, invest in relationships, and remove friction for dealers are the ones that earn trust and repeat business.

Human engagement remains essential. While digital tools drive information, confidence, and discovery, pros still rely on human support to solve problems quickly. Fast response times, accessible representatives, and real-time issue resolution directly influence brand choice and loyalty.

Other top priorities for builders in 2026 will be:

- Tightly controlling project costs

- Tightly controlling project timelines

- Managing project quality and client expectations, while optimizing the efficiency of crews to compensate for labor challenges

- Securing new business from a smaller pool of prospects and with increased competition

As homeowners are particularly budget sensitive because of economic conditions, they are making tradeoffs on where and how they spend, and contractors must respond. Manufacturers and suppliers must offer a breadth of prices and value propositions to accommodate a range of needs.

Building materials manufacturers and suppliers must be prepared to help Pros with effective offerings, quality product choices at competitive prices, convenient distribution channels, and customer-centric marketing methods. You will increase pro loyalty to your brand by tailoring your go-to-market strategy to meet builders where they’re at during any challenging economic conditions that force builders to make trade-offs in their supplier and product selections.

For building product and home improvement manufacturers and suppliers this environment demands a shift from growth-at-all-costs to precision, responsiveness, and value clarity. Price and value transparency are critical. Homeowners are budget sensitive, and contractors are under cost pressure. Building Product Manufacturers and Suppliers that offer clear good-better-best assortments, transparent pricing, and strong value messaging will be better positioned to support trade-down behavior without sacrificing volume.

Availability, reliability, and support matter more than ever. Contractors consistently cite product availability, delivery timelines, and quality as top frustrations. Manufacturers and Suppliers that minimize friction through dependable supply, accurate information, and responsive service become preferred partners in a competitive professional environment.

Alignment with contractor workflows is a differentiator. As pros navigate delayed jobs, tighter schedules, and customer uncertainty, suppliers that meet them where they are-through flexible ordering, clear documentation, and proactive communication-help stabilize their businesses.

In a market defined by uncertainty rather than decline, suppliers that reduce risk, simplify decisions, and reinforce trust will not only weather current conditions but emerge stronger as demand gradually reaccelerates.

Gaining Insight for Building Products Manufacturers and Suppliers

To learn more about what contractors are doing and thinking when it comes to purchasing building materials in 2026, request access to the latest Construction and Remodeling Industry Drivers and Forecast Study from The Farnsworth Group.

Our team also can work with you to conduct customized market research for your business. Whether your focus is on selling to new home builders, remodelers, or specialty tradespeople, our researchers are equipped to connect with hard-to-reach pros for custom market research studies to get you the insights that you need to drive business forward.