The major household appliance sector has a sizable influence on the home improvement industry and is heavily impacted by the new home market. Because products within this category tend to have a higher price point, they account for the highest median spend among customers.

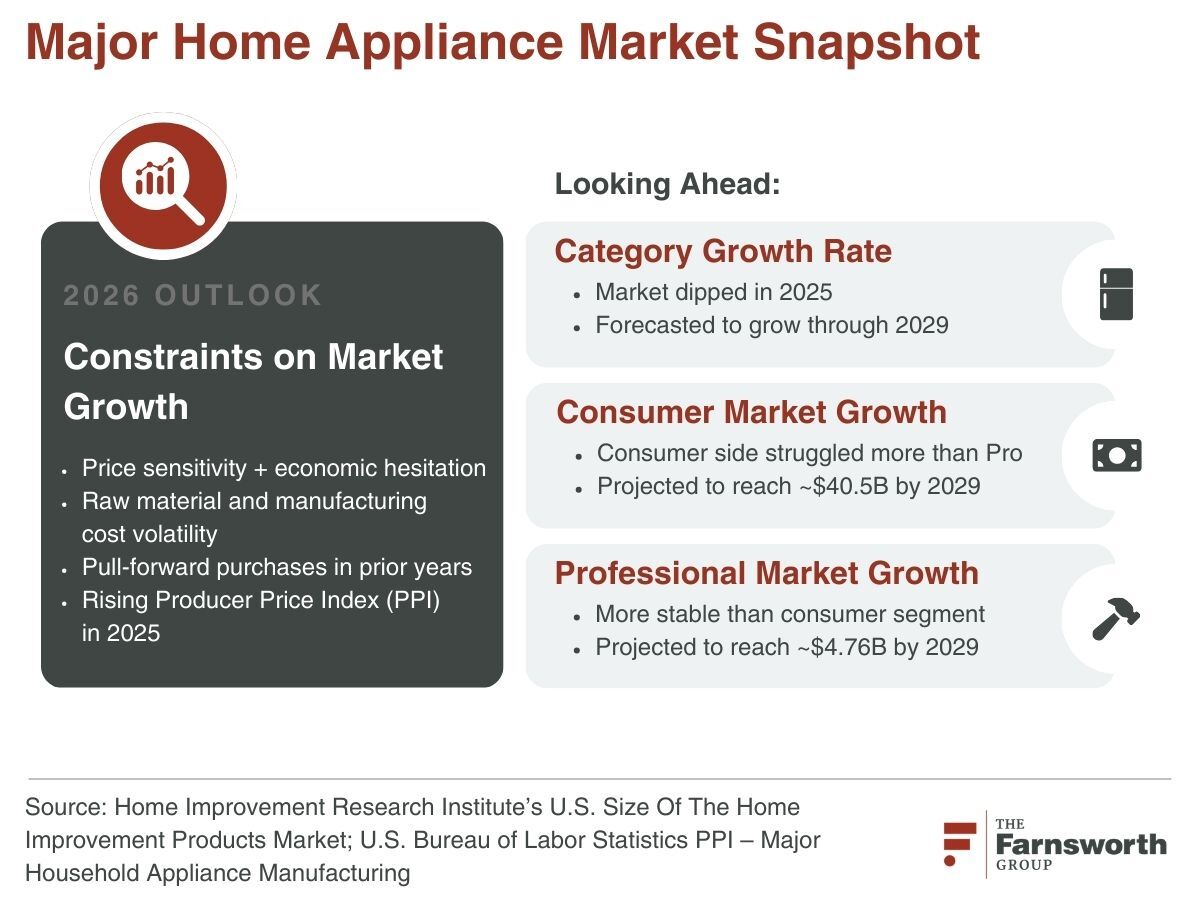

Like other product categories, large home appliances struggled in terms of market growth in 2025 for a variety of reasons, from availability constraints and the fluctuating costs of raw materials to tempered consumer confidence and pull-forward purchases over the past two to three years. Looking ahead into 2026 and beyond, the market forecast is a bit more positive.

Currently customers continue to be weighed down with financial and economic concerns, which translates into more price sensitivity and hesitancy to conduct large home improvement projects or make large purchases in general. Manufacturers and retailers must be acutely aware of current trends in the major home appliance market and the preferences, challenges, and purchase motivators of consumers in order to capture some of the projected growth over the next few years.

What is the Major Home Appliance Market Size in 2026?

Major household appliances include items like:

- Refrigerators

- Freezers

- Dishwashers

- Ranges

- Microwaves

- Washers and dryers

This product category doesn’t include dehumidifiers, room air-conditioners, or outdoor gas grills.

In 2025, the major home appliances market in the U.S. was valued at approximately $42.7 billion, according to data from Mordor Intelligence. This product category is estimated to grow from about $43.95 billion in 2026 to $ 50.6 billion by 2031, a compound annual growth rate (CAGR) of roughly 2.86%.

In general, it’s been the consumer side of the market struggling more than the professional market, but both are projected to have a similar growth rate over the next few years. The consumer market is projected to grow to about $40.5 billion in the U.S. by 2029, while the professional market will hover about $4.76 billion.

As per the U.S. Bureau of Labor Statistic’s Producer Price Index (PPI) for Major Household Appliance Manufacturing, there was a huge spike in prices within the industry in mid-2021 to mid-2022 before leveling off through the end of 2024. From early 2025 onward, manufacturing prices for major household appliances have dramatically increased, once again. The index jumped from 165.6 in January 2025 to approximately 174 in December 2025.

The major players in the household appliance market—in terms of both dollar share and unit share—are Samsung, LG, General Electric, and Whirlpool.

What Trends Impact the Outlook for Major Appliance Sales?

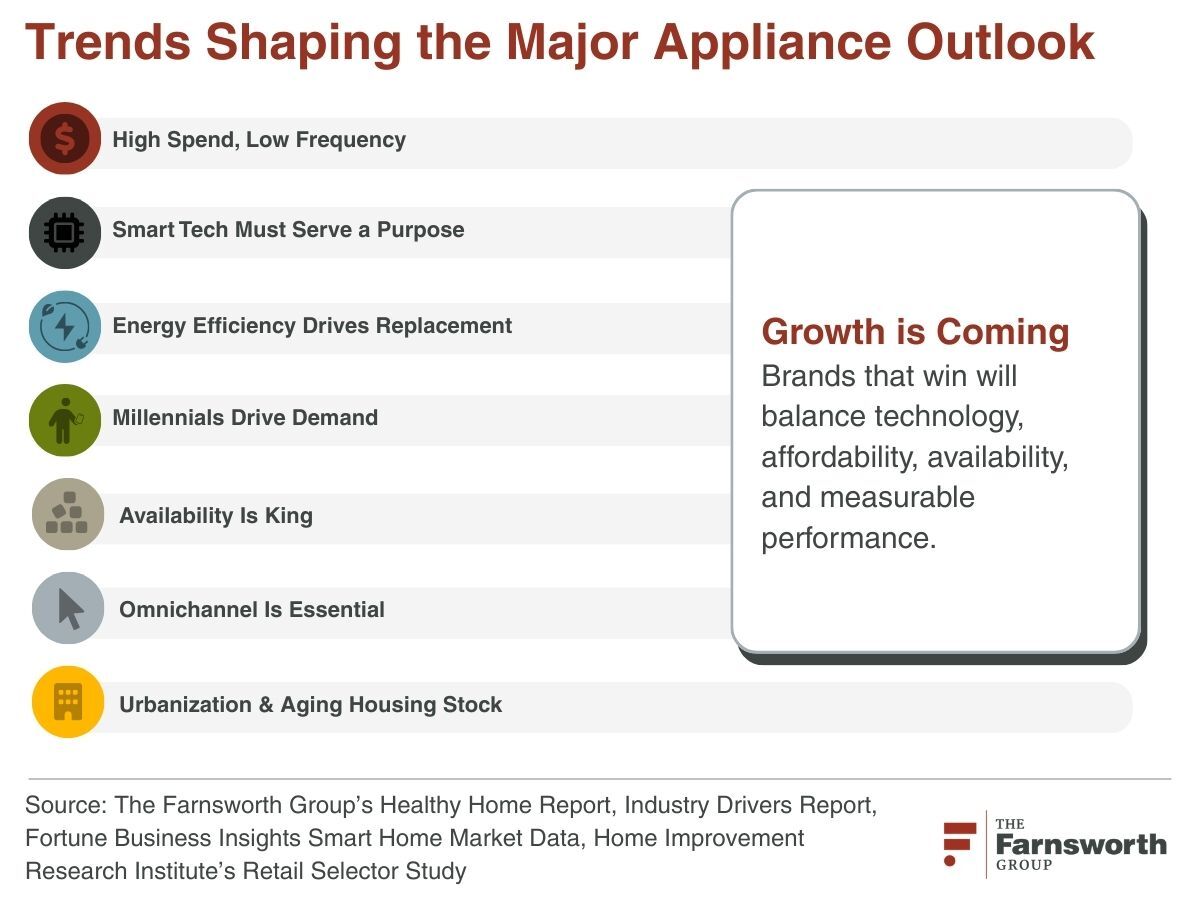

To prepare for the expected growth in the large home appliance market over the next couple of years, manufacturing and retail brands can use data about customer behaviors and preferences, from a desire for energy efficient and high-functioning households to an increasing willingness to select a non-familiar brand.

Here is a look at some of the trends in the home appliance industry and how they will impact the market’s growth over the next few years:

1. Refrigerators Retain Highest Markest Share by Product

Since 2019, we've witnessed a significant spike in how much U.S. households spend on all types of home appliances in a given year, based on data from the U.S. Bureau of Economic Analysis via FRED. Major home appliances account for more than half of these expenditures. Meanwhile, refrigerators maintained the largest the largest market share by product, or 24.7%, in 2025, based on research from Mordor Intelligence. Recurring energy-upgrade cycles and demand for smart refrigerators with high-tech features, as well as consistent food storage and preservation needs, contribute to that dominance. Additionally, the highest price point for major household appliance, in general, may contribute to growth in the overall market between 2026 and 2029.

2. Adoption of Smart Home Appliances is Rising

As smart devices become further integrated and easier to use, homeowners are increasingly drawn to the convenience and interoperability of smart appliances within the residential setting. In 2026, nearly half of U.S. households have at least one smart home device, and the smart home market is projected to grow both domestically and abroad over the next six to eight years, according to Fortune Business Insights.

When it comes to large household appliances, some examples of smart features include:

- Refrigerators that alert the homeowner if a door is left open or the help with inventory management

- Wash machines that notify your smart phone when a cycle is done

- Faucets that measure how much water is required

- Ovens that you can turn on to preheat remotely and that will turn off when food is ready

More advanced features allow remote programming for cooking and ordering food as well as remote monitoring and self-diagnosis of the appliance. Industry stakeholders should explore the potential to refine the technological aspects of major home appliances and enhance interoperability to meet the demand from customers.

However. the key to performing well in this market will be to prioritize simplicity and a clear purpose—not just incorporating tech for tech’s sake. Smart features must help customers meet their needs in terms of energy efficiency, saving time, reducing stress, and promoting health and wellness.

3. Energy Efficiency and Sustainability Matter to Customers

Major household appliances have a significant impact on a residence’s energy consumption. Consequently, property owners—whether homeowners or landlords who manage multi-family housing—are increasingly conscientious about selecting models that are energy efficient.

The Relationship Between Smart Technology and Energy Efficiency

The demand for energy optimization is expected to contribute to the growth in the major home appliance market as individuals consider replacing older, less-efficient models for newer products engineered to meet today’s standards. Certain consumer segments are driven by sustainability and environmental factors, not just a return on their investment. Much of the smart technology mentioned above is related to this goal: making appliances more environmentally friendly and helping households better manage (and conserve) their energy usage. The U.S. Department of Energy’s Appliance and Equipment Standards Program and other government regulations also influence the major home appliances market in the U.S. Homeowners looking to lower utility bills and reduce energy consumption are actively seeking ENERGY STAR-certified appliances and exploring government incentives to help offset costs.

Customers Expect ROI on Energy Efficient Upgrades

According to our recent Healthy & Safe Home and Environmental & Energy Performance Attitudes report, produced in conjunction with the Harvard Joint Center for Housing Studies, younger, wealthier, and educated homeowners have greater desires to help the environment and see home improvements and upgrades as a means to do so. However, they expect a return on investment (ROI) in the form of costs or comfort benefits. As a manufacturer, it’s important to communicate measurable returns or product performance as much as sentimental returns.

4. Drive from the Millennial Market

As a demographic, Millennials are an important driver in the home appliance market. This age group is actively buying new or renovating existing homes to accommodate expanding, and even multi-generational, families. They also have more purchasing power at this time. Large appliance brands and retailers should consider how they can target this demographic more effectively and build their loyalty. This includes adapting marketing strategies and understanding millennials’ preferred channels and shopping behaviors. This large generation can be diverse, with some in their mid- to late 40s earning a high income versus those just now turning 30 with less to invest. Contractors are no different, with some serving luxury and others entry level.

And while millennials account for a large customer base, Gen Z homeowners can’t be ignored, either, as they acquire more buying power in the housing and home improvement markets. Defining customer segments is critical to knowing what influences a purchase—where, when and how—and tailoring your offerings and distribution strategies accordingly.

5. Brand Loyalty has been Decreasing

When it comes to brand loyalty, customers are more likely to be motivated by cost and availability for major home appliances. Whether they’re looking for a product for a new home or replacing an older, defunct unit in their existing home, there is typically a sense of urgency around choosing a product like a dishwasher, stove, or wash machine.

Availability and Costs are Major Factors in Brand Shifting

Customers are willing to overlook brand loyalty or try one that is unfamiliar if they can find a replacement product from a different brand more quickly or conveniently—and within their budget. Part of this behavior may be a residual effect of the COVID-19 pandemic, when supply chain issues, backlog, and other economic pressures motivated property owners and professionals to be more willing to try new brands. Many homeowners also prioritize product availability and price over brand loyalty, motivating their willingness to shop around.

For home appliance brands, there is a growing need to cultivate loyalty by offering a superior customer experience, as well as addressing supply chain disruptions that negatively affect product availability.

6. Expanding In-Store and Online Purchase Channels

About two-thirds of customers still make their purchase of a major appliance at a physical store, with home centers being the preferred retailer type. They appreciate the opportunity to examine products in person, check out the features, and speak with professionals at retail locations. However, online purchases account for about 20% and buying online and picking up in-store accounts for another 13% of other purchases.

Online Suppliers have Growing Presence in Home Improvement Products Market

Looking forward, customers have several options for where and how to purchase large home appliances. Online channels—through Amazon or even Best Buy and Costco—can be appealing because of their convenience, the promise of home delivery services, and competitive pricing. While online channels don’t account for the same percentage of sales as they did during the COVID-19 pandemic, this purchase method maintains a higher rate than in 2018.

Omni-Channel Business Strategy is Key

Smaller local and regional distributors are wise to maintain a robust online presence that is able to compete, whether that’s by offering similar features, such as integrated product comparison tools, or by offering superior customer services, targeted marketing, and customer follow-up. Meanwhile, some brands, like Samsung, have opened experience retail stores to let customers who prefer brick-and-mortar channels to see and test products in person.

7. Urbanization and Changes in the Housing Market

Growth in the major home appliance market is also likely to be influenced by various housing trends we’re witnessing across the country. For example, the median age of owner-occupied homes is now 43 years, rising steadily since the Great Recession as a result of underbuilding of new homes and older homes remaining in inventory. The age of housing stock varies by region with the oldest homes in the Northeast and newest homes in the South.

Maintenance and Upgrades Drive Remodeling Market

Older homes need more maintenance and upgrades, driving growth in the remodeling, repair, and maintenance market. Remodeling may surpass new construction as the housing stock continues to age, and this may be beneficial for major home appliances sales in the forecast period. Replacing older appliances is one way that homeowners can maintain the comfort and convenience of their current housing situation, and overall quality of life, until they are able to relocate.

The housing inventory suggests the lock-in effect is beginning to loosen, yet many buyers hesitate to make a move until mortgage rates fall under 6%, according to findings in our Construction and Remodeling Industry Drivers & Forecast.

Multi-Family Housing is Filling the Gap on Low Inventory

Additionally, multi-family (MF) starts have seen a rebound in 2025 in response to the low affordability of single-family homes and high new home inventory. It’s expected that new projects will be undertaken in various metropolitan areas and low-density suburbs outside large cities as a result of significant rent growth and tight vacancies over the past few years. These types of projects provide an opportunity for large household appliance brands within the market as well, and brands can capitalize on the opportunity by developing products that fit the need for compact, multifunctional devices.

Using Custom Research to Inform Business Strategies

Knowing the trends shaping the home appliance market can help you identify new competition, as well as new opportunities, and make business decisions accordingly. While several trends are happening on a larger scale, manufacturing and retail brands in the home improvement industry can also benefit by gaining more customized research and insights about their particular market.

That’s where our building product research experts at The Farnsworth Group come in. We have extensive experience in the home improvement industry and helping stakeholders create successful customer, product, brand and market strategies backed by our proven market research solutions. Learn more about commissioning custom market research to make the right call to win with your end-users, channel customers, and in the appliances market overall.

By Eric Voyer

Director and Senior Consultant

Eric brings nearly 30 years of experience in market research, business development, and strategic consulting within the home improvement, building products, and outdoor industries. He spent decades in syndicated research for consumer durables, where he helped leading brands turn complex data into actionable insights that drive growth. Eric's expertise spans both quantitative and qualitative methodologies. At The Farnsworth Group, Eric focuses on client engagement, project design, and strategic storytelling to ensure insights lead to clear, confident decisions.

Originally from Orlando and now based in Louisville, KY, Eric studied Business at Transylvania University, where he also competed as a collegiate goalkeeper. Outside of work, Eric still enjoys playing soccer, loves to Ski and Scuba and has a new passion for playing ice hockey.